509 Payment of Fees [R-01.2024]

The latest fee schedule is available by contacting the USPTO at 1-800-PTO(786)-9199 or (571) 272-1000, or on the USPTO webpage at www.uspto.gov/Fees.

37 CFR 1.22 Fees payable in advance.

- (a) Patent fees and charges payable to the United States Patent and Trademark Office are required to be paid in advance; that is, at the time of requesting any action by the Office for which a fee or charge is payable with the exception that under § 1.53 applications for patent may be assigned a filing date without payment of the basic filing fee.

- (b) All fees paid to the United States Patent and Trademark Office must be itemized in each individual application, patent, or other proceeding in such a manner that it is clear for which purpose the fees are paid. The Office may return fees that are not itemized as required by this paragraph. The provisions of § 1.5(a) do not apply to the resubmission of fees returned pursuant to this paragraph.

37 CFR 1.23 Method of payment.

- (a) All payments of money required for United States Patent and Trademark Office fees, including fees for the processing of international applications (§ 1.445), shall be made in U.S. dollars and in the form of a cashier’s or certified check, Treasury note, national bank notes, or United States Postal Service money order. If sent in any other form, the Office may delay or cancel the credit until collection is made. Checks and money orders must be made payable to the Director of the United States Patent and Trademark Office. (Checks made payable to the Commissioner of Patents and Trademarks will continue to be accepted.) Payments from foreign countries must be payable and immediately negotiable in the United States for the full amount of the fee required. Money sent to the Office by mail will be at the risk of the sender, and letters containing money should be registered with the United States Postal Service.

- (b) Payments of money required for United States Patent and Trademark Office fees may also be made by credit card, except for replenishing a deposit account. Payment of a fee by credit card must specify the amount to be charged to the credit card and such other information as is necessary to process the charge, and is subject to collection of the fee. The Office will not accept a general authorization to charge fees to a credit card. If credit card information is provided on a form or document other than a form provided by the Office for the payment of fees by credit card, the Office will not be liable if the credit card number becomes public knowledge.

- (c) A fee transmittal letter may be signed by a juristic applicant or patent owner.

37 CFR 1.26 Refunds.

- (a) The Director may refund any fee paid by mistake or in excess of that required. A change of purpose after the payment of a fee, such as when a party desires to withdraw a patent filing for which the fee was paid, including an application, an appeal, or a request for an oral hearing, will not entitle a party to a refund of such fee. The Office will not refund amounts of twenty-five dollars or less unless a refund is specifically requested, and will not notify the payor of such amounts. If a party paying a fee or requesting a refund does not provide the banking information necessary for making refunds by electronic funds transfer (31 U.S.C. 3332 and 31 CFR part 208), or instruct the Office that refunds are to be credited to a deposit account, the Director may require such information, or use the banking information on the payment instrument to make a refund. Any refund of a fee paid by credit card will be by a credit to the credit card account to which the fee was charged.

- (b) Any request for refund must be filed within two years from the date the fee was paid, except as otherwise provided in this paragraph or in § 1.28(a). If the Office charges a deposit account by an amount other than an amount specifically indicated in an authorization (§ 1.25(b)), any request for refund based upon such charge must be filed within two years from the date of the deposit account statement indicating such charge, and include a copy of that deposit account statement. The time periods set forth in this paragraph are not extendable.

- (c) If the Director decides not to institute a reexamination

proceeding in response to a request for reexamination or supplemental examination,

fees paid with the request for reexamination or supplemental examination will be

refunded or returned in accordance with paragraphs (c)(1) through (c)(3) of this

section. The reexamination requester or the patent owner who requested a

supplemental examination proceeding, as appropriate, should indicate the form in

which any refund should be made ( e.g., by check, electronic funds transfer,

credit to a deposit account). Generally, refunds will be issued in the form that

the original payment was provided.

- (1) For an ex parte reexamination request, the ex parte reexamination filing fee paid by the reexamination requester, less the fee set forth in § 1.20(c)(7), will be refunded to the requester if the Director decides not to institute an ex parte reexamination proceeding.

- (2) For an inter partes reexamination request, a refund of $7,970 will be made to the reexamination requester if the Director decides not to institute an inter partes reexamination proceeding.

- (3) For a supplemental examination request, the fee for reexamination ordered as a result of supplemental examination, as set forth in § 1.20(k)(2), will be returned to the patent owner who requested the supplemental examination proceeding if the Director decides not to institute a reexamination proceeding.

Where the Office has notified an applicant, in writing, that a fee is due and has specified a particular dollar amount for that fee, if the applicant timely submits the specified fee amount in response to the notice, the applicant should be considered to have complied with the notice so as to avoid abandonment of the application. If the fee paid by the applicant is insufficient, either because the notice specified an incorrect dollar amount for the fee or because of a fee increase effective after the mailing of the notice and before payment of the fee by the applicant, the applicant should be notified in writing by the Office of the fee insufficiency and given a new time period in which to submit the remaining balance. The written notification of the fee insufficiency should set forth the reason (i.e., the fee amount indicated by the Office in the earlier notice was incorrect or the fees have increased since the earlier notice was mailed) why applicant is being required to submit an additional fee.

I. ITEMIZATION AND APPLICATION OF FEES37 CFR 1.22(b) sets forth that fees must be itemized in such a manner that it is clear for which purpose fees are paid. The Office may return fees that are not itemized. The intent of the fee itemization requirement is to encourage a better explanation by applicants of how fees being paid are to be applied by the Office. This will allow Office employees to properly account for the fees being paid by applicants. It should be noted that the language of 37 CFR 1.22 is not intended to create a problem when it is clear what fee is needed. A reference to “filing fee(s)” would be sufficient to cover filing fees (including search and examination fees) of all different types of applications and all types of claims. Further, in a paper submitted on a date later than the actual filing date, the reference to “filing fee(s)” would also be sufficient to cover the surcharge under 37 CFR 1.16, as the surcharge is also required to make the application complete. A reference to “any corresponding fee under 37 CFR 1.16” would be sufficient to cover any fee (e.g., surcharge, application size fee, excess claims fees) under 37 CFR 1.16. In a petition for an extension of time filed without a specifically itemized fee, but with a general authorization to charge a deposit account, it is clear that a fee for an extension of time is needed and the deposit account should be charged the appropriate extension of time fee.

In situations in which a payment submitted for the fees due on filing in a nonprovisional application filed under 35 U.S.C. 111(a) is insufficient and the applicant has not specified the fees to which the payment is to be applied, the Office will apply the payment in the following order until the payment is expended:

- (1) the basic filing fee (37 CFR 1.16(a), (b), (c), or (e));

- (2) the non-electronic filing fee (37 CFR 1.16(t));

- (3) the non-DOCX fee (37 CFR 1.16(u))

- (4) the application size fee (37 CFR 1.16(s));

- (5) the late filing surcharge (37 CFR 1.16(f));

- (6) the processing fee for an application filed in a language other than English (37 CFR 1.17(i));

- (7) the search fee (37 CFR 1.16(k), (l), (m), or (n));

- (8) the examination fee (37 CFR 1.16(o), (p), (q), or (r)); and

- (9) the excess claims fee (37 CFR 1.16(h), (i), and (j)).

In situations in which a payment submitted for the fees due on filing in a provisional application filed under 35 U.S.C. 111(b) is insufficient and the applicant has not specified the fees to which the payment is to be applied, the Office will apply the payment in the following order until the payment is expended:

- (1) the basic filing fee (37 CFR 1.16(d));

- (2) the application size fee (37 CFR 1.16(s)); and

- (3) the late filing surcharge (37 CFR 1.16(g)).

See also MPEP § 607.

37 CFR 1.492 specifies the required fees for international applications entering the national stage under 35 U.S.C. 371. The basic national fee must be paid prior to the expiration of 30 months from the priority date to avoid abandonment of the international application as to the United States. This time period is not extendable. 37 CFR 1.495(a) - (b). This is distinguished from U.S. national application filings under 35 U.S.C. 111(a) in which the basic filing fee due on filing may be later accepted with a surcharge. Accordingly, in situations in which a payment of fees has been made in a national stage application prior to the expiration of 30 months from the priority date, but the applicant has not specified a sufficient amount for the payment of the basic national fee, the Office will apply the payment first to the basic national fee regardless of whether the applicant specified the fees to which the payment is to be applied.

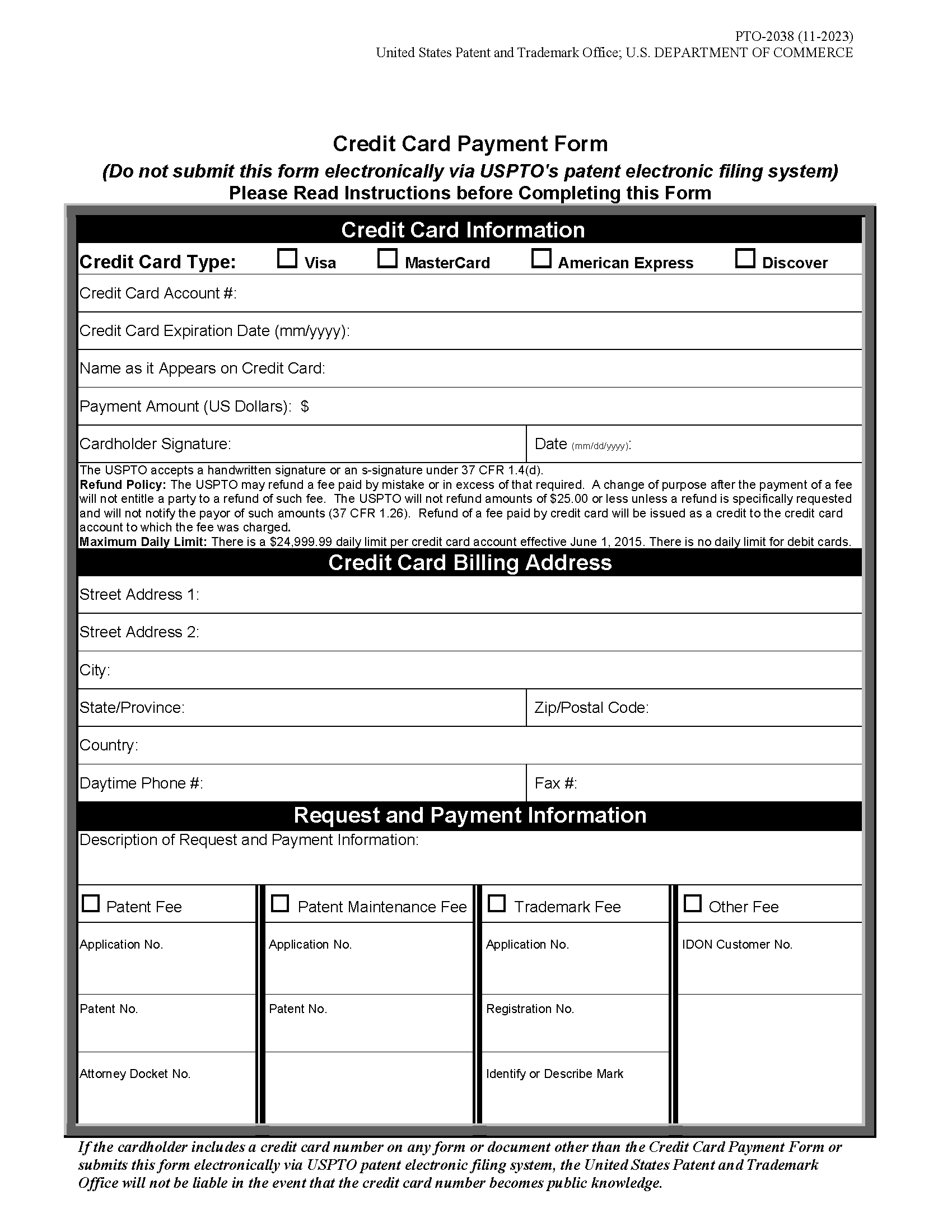

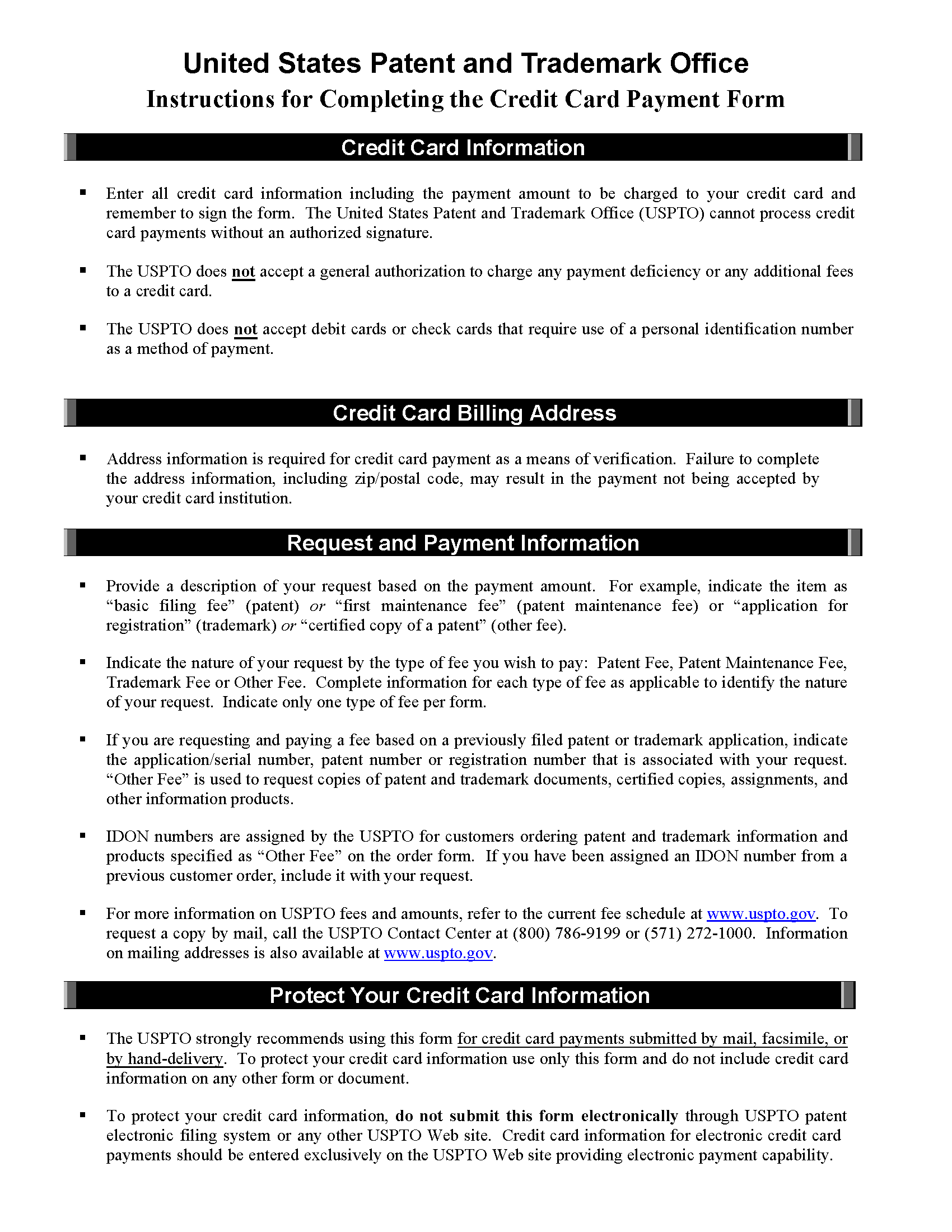

II. PAYMENT BY CREDIT CARD37 CFR 1.23 permits payment of any patent process fee, trademark process fee, or information product fee by credit card, subject to actual collection of the fee. The Office currently accepts charges to the following credit cards: AMERICAN EXPRESS®, DISCOVER®, MASTER CARD®, and VISA®.

Individual credit card payments to the Office, as well as multiple credit card payments made to U.S. Government entities on the same day, may not exceed the transaction maximum imposed by the Department of the Treasury. Effective June 1, 2015, the credit card transaction maximum is $24,999.99 as specified in section 7045 of the “Treasury Financial Manual.” Any credit card payment exceeding the transaction maximum may be rejected. This transaction maximum applies only to credit cards; there is no daily limit for debit cards, deposit account charges, or other forms of payment accepted by the Office. The currently applicable credit card transaction maximum is stated on the Credit Card Payment Form (PTO-2038).

Credit Card Payment Form (PTO-2038) should be used when paying a patent process or trademark process fee (or the fee for an information product) by credit card, unless the payment is being made using the USPTO patent electronic filing system. The credit card payment form is not required (and should not be used) when making a credit card payment via the USPTO patent electronic filing system. Form PTO-2038 may be downloaded at www.uspto.gov/PatentForms. The Office will not include the Credit Card Payment Form (PTO-2038) among the records open to public inspection in the file of a patent, trademark registration, or other proceeding. The Office does not require customers to use this form when paying a patent process or trademark process fee by credit card. If a customer provides a credit card charge authorization in another form or document (e.g., a communication relating to the patent or trademark), the credit card information may become part of the record of an Office file that is open to public inspection. Thus, failure to use the Credit Card Payment Form (PTO-2038) when submitting a credit card payment may result in the credit card information becoming part of the record of an Office file that is open to public inspection.

35 U.S.C. 42(d) and 37 CFR 1.26 (which concern refund of patent and trademark fees) also apply to requests for refund of fees paid by credit card. Any refund of a fee paid by credit card will be by a credit to the credit card account to which the fee was charged. See 37 CFR 1.26(a).

See MPEP § 607.02 for returnability of fees.

Any payment of a patent process or trademark process fee by credit card must be in writing (see 37 CFR 1.2), and preferably submitted via the USPTO patent electronic filing system, or if filed in paper, on the Credit Card Payment Form (PTO-2038). If a Credit Card Payment Form or other document authorizing the Office to charge a patent process or trademark process fee to a credit card does not contain the information necessary to charge the fee to the credit card, the customer must submit a revised Credit Card Payment Form or document containing the necessary information. Office employees will not accept oral (telephonic) instructions to complete the Credit Card Payment Form or otherwise charge a patent process or trademark process fee (as opposed to information product or service fees) to a credit card.

Credit card payment submissions made on the USPTO website at www.uspto.gov must include the 3-digit or 4-digit security code associated with the credit card in addition to the credit card number. The security code will not be required when the paper Credit Card Payment Form (PTO-2038) or other written authorization is submitted.

The security code is part of an authentication procedure established by credit card companies to further efforts towards reducing fraudulent or unauthorized credit card use for Internet payment transactions. The security code must be entered at the time of the Internet payment transaction to verify that the physical card is in the cardholder’s possession. The security code appears on all major credit cards and is not part of the credit card number itself. Each credit card company has its own name for the security code (such as CVV, CVV2, CVC2 or CID), but it functions the same for all major card types.

On DISCOVER®, MASTERCARD®, and VISA® credit cards, the security codes is a 3-digit code that is printed on the back of the card, often following the credit card number digits. For AMERICAN EXPRESS® credit cards, the security code is a 4-digit code that is printed on the front of the cards. If you cannot read the security code, you will have to contact the financial institution that issued your credit card.

509.01 Deposit Accounts [R-01.2024]

37 CFR 1.25 Deposit accounts.

- (a) For the convenience of attorneys, and the general public in paying any fees due, in ordering services offered by the Office, copies of records, etc., deposit accounts may be established in the Patent and Trademark Office upon payment of the fee for establishing a deposit account § 1.21(b)(1). A minimum deposit of $1,000 is required for paying any fee due or in ordering any services offered by the Office. However, a minimum deposit of $300 may be paid to establish a restricted subscription deposit account used exclusively for subscription order of patent copies as issued. At the end of each month, a deposit account statement will be rendered. A remittance must be made promptly upon receipt of the statement to cover the value of items or services charged to the account and thus restore the account to its established normal deposit value. An amount sufficient to cover all fees, services, copies, etc., requested must always be on deposit. Charges to accounts with insufficient funds will not be accepted. A service charge (§ 1.21(b)(2)) will be assessed for each month that the balance at the end of the month is below $1,000. For restricted subscription deposit accounts, a service charge (§ 1.21(b)(3)) will be assessed for each month that the balance at the end of the month is below $300.

- (b) Filing, issue, appeal, international-type search report, international application processing, international design application fees, petition, and post-issuance fees may be charged against these accounts if sufficient funds are on deposit to cover such fees. A general authorization to charge all fees, or only certain fees, set forth in §§ 1.16 through 1.18 to a deposit account containing sufficient funds may be filed in an individual application, either for the entire pendency of the application or with a particular paper filed. A general authorization to charge fees in an international design application set forth in § 1.1031 will only be effective for the transmittal fee (§ 1.1031(a)). An authorization to charge fees under § 1.16 in an international application entering the national stage under 35 U.S.C. 371 will be treated as an authorization to charge fees under § 1.492. An authorization to charge fees set forth in § 1.18 to a deposit account is subject to the provisions of § 1.311(b). An authorization to charge to a deposit account the fee for a request for reexamination pursuant to § 1.510 or 1.913 and any other fees required in a reexamination proceeding in a patent may also be filed with the request for reexamination, and an authorization to charge to a deposit account the fee for a request for supplemental examination pursuant to § 1.610 and any other fees required in a supplemental examination proceeding in a patent may also be filed with the request for supplemental examination. An authorization to charge a fee to a deposit account will not be considered payment of the fee on the date the authorization to charge the fee is effective as to the particular fee to be charged unless sufficient funds are present in the account to cover the fee.

- (c) A deposit account holder may replenish the deposit account by

submitting a payment to the United States Patent and Trademark Office. A

payment to replenish a deposit account must be submitted by one of the methods

set forth in paragraphs (c)(1), (c)(2), (c)(3), or (c)(4) of this section.

- (1) A payment to replenish a deposit account may be submitted

by electronic funds transfer through the Federal Reserve Fedwire System,

which requires that the following information be provided to the deposit

account holder’s bank or financial institution:

- (i) Name of the Bank, which is Treas NYC (Treasury New York City);

- (ii) Bank Routing Code, which is 021030004;

- (iii) United States Patent and Trademark Office account number with the Department of the Treasury, which is 13100001; and

- (iv) The deposit account holder’s company name and deposit account number.

- (2) A payment to replenish a deposit account may be submitted by electronic funds transfer over the Office’s Internet website (www.uspto.gov).

- (3) A payment to replenish a deposit account may be addressed to: Mail Stop Deposit Accounts, Director of the United States Patent and Trademark Office, P.O. Box 1450, Alexandria, Virginia 22313-1450.

- (1) A payment to replenish a deposit account may be submitted

by electronic funds transfer through the Federal Reserve Fedwire System,

which requires that the following information be provided to the deposit

account holder’s bank or financial institution:

An overdrawn account will be immediately suspended and no charges will be accepted against it until a proper balance is restored, together with a payment of $10 (37 CFR 1.21(b)(1)) to cover the work done by the U.S. Patent and Trademark Office incident to suspending and reinstating the account and dealing with charges which may have been made in the meantime.

If there is an authorization to charge the basic filing fee (37 CFR 1.16(a), (b), (c), (d), or (e)) to a deposit account which is overdrawn or has insufficient funds, a surcharge (37 CFR 1.16(f)) is required in addition to payment of the basic filing fee (37 CFR 1.16(a), (b), (c), (d), or (e)). For applications filed on or after July 1, 2005, which have been accorded a filing date under 37 CFR 1.53(b) or (d), if there is an authorization to charge any of the basic filing fee, the search fee, or the examination fee to a deposit account which is overdrawn or has insufficient funds, a surcharge under 37 CFR 1.16(f) is required in addition to payment of the required fee(s). Failure to timely pay the filing fee and surcharge will result in abandonment of the application.

It is expected, however, that reasonable precautions will be taken in all cases to avoid overdrafts, and if an account is suspended repeatedly it will be closed.

Similarly, because of the burden placed on the U.S. Patent and Trademark Office incident to the operation of deposit accounts, a charge of $10 (37 CFR 1.21(b)(1)) will be made for opening each new account.

I. DEPOSIT ACCOUNT AUTHORIZATIONS37 CFR 1.25(b) states that:

A general authorization to charge all fees, or only certain fees, set forth in §§ 1.16 to 1.18 to a deposit account containing sufficient funds may be filed in an individual application, either for the entire pendency of the application or with respect to a particular paper filed.

Authorized users for a deposit account must be listed in Financial Manager as authorized fee payers. Office personnel will accept obvious variations of the given name (first name or middle name) provided that the last or family name matches the authorized fee payer’s last name. Where the fee payer’s last name in a signed fee authorization document does not match any of the authorized fee payers for the deposit account which is being relied upon to pay a fee, the fee payment may be delayed or rejected.

Many applications contain broad language authorizing any additional fees which might have been due to be charged to a deposit account. The U.S. Patent and Trademark Office will interpret such broad authorizations to include authorization to charge to a deposit account fees set forth in 37 CFR 1.16, and 1.17. Fees under 37 CFR 1.19, 1.20, and 1.21 will not be charged as a result of a general authorization under 37 CFR 1.25 except to cover the processing fee under 37 CFR 1.21(m) in the event a check or credit card payment is refused or charged back by a financial institution. Fees under 37 CFR 1.18 will not be charged as a result of a preauthorization of issue fee payment.

An authorization to charge fees relating only to a specific paper, could read “The Director is hereby authorized to charge any fees under 37 CFR 1.16 and 1.17 which may be required by this paper to Deposit Account No.________.” Such an authorization would cover situations in which a check to cover a filing and/or a processing fee under 37 CFR 1.16 and 1.17 was omitted or was for an amount less than the amount required. An authorization covering any omission or deficiency in a check or credit card payment applies to the processing fee under 37 CFR 1.21(m) in the event a check or credit card payment is refused or charged back by a financial institution, regardless of whether such deposit account authorization is limited to other fees (e.g., fees under 37 CFR 1.16 and 1.17). If a check or credit card payment for the issue fee is refused or charged back by a financial institution, the application may be held abandoned for failure to pay the issue fee within the statutory period for reply. See MPEP § 1306.

It is extremely important that the authorization be clear and unambiguous. If applicants file authorizations which are ambiguous and deviate from the usual forms of authorizations, the Office may not interpret the authorizations in the manner applicants intend and may return the fees. As a result, applicants could be subject to further expenses, petitions, etc. in order to have a particular fee charged to a deposit account (which was not charged as intended) or to resubmit a fee(s) due to an ambiguous authorization.

The Office will treat a deposit account authorization to charge "the filing fee" as an authorization to charge the following applicable fees under 37 CFR 1.16: basic filing fee; search fee; examination fee; any excess claims fees; any application size fee; and any non-electronic filing fee (see 37 CFR 1.16(t)). The Office will treat a deposit account authorization to charge "the basic filing fee" as an authorization to charge the following applicable fees under 37 CFR 1.16: basic filing fee; search fee; and examination fee. Any deposit account authorization to charge the filing fee but not the search fee or examination fee must specifically limit the authorization by reference to one or more paragraphs (a) - (e) of 37 CFR 1.16.

37 CFR 1.25(b) provides that an authorization to charge fees under 37 CFR 1.16 (which relates to national application filing fees) in an application filed under 35 U.S.C. 371 will be treated as an authorization to charge fees under 37 CFR 1.492 (which relates to national stage fees). Papers filed for the purpose of entering the national stage under 35 U.S.C. 371 and 37 CFR 1.495 that include an authorization to charge fees under 37 CFR 1.16 are treated by the Office as an authorization to charge fees under 37 CFR 1.492 since: (1) timely payment of the appropriate national fee under 37 CFR 1.492 is necessary to avoid abandonment of the application as to the United States; and (2) the basic filing fee under 37 CFR 1.16 is not applicable to such papers or applications.

37 CFR 1.25(b) sets forth that fees in an international design application may be charged to a deposit account. A general authorization to charge fees in an international design application set forth in 37 CFR 1.1031 will only be effective for the transmittal fee (37 CFR 1.1031(a)). The international fees set forth in 37 CFR 1.1031, other than the transmittal fee set forth in 37 CFR 1.1031(a), are not required to be paid to the Office as an office of indirect filing. See 37 CFR 1.1031(d).

As provided in 37 CFR 1.311(b), an authorization to charge the issue fee (37 CFR 1.18) to a deposit account may be filed in an individual application only after the mailing of the notice of allowance. 37 CFR 1.25(b) also makes clear that a general authorization made prior to the mailing of a notice of allowance does not apply to issue fees under 37 CFR 1.18.

In addition, a general authorization does not apply to document supply fees under 37 CFR 1.19, such as those required for certified copies, to post issuance fees under 37 CFR 1.20, such as those required for maintenance fees, or to miscellaneous fees and charges under 37 CFR 1.21, such as assignment recording fees.

II. DEPOSIT ACCOUNT REPLENISHMENTS37 CFR 1.25(c) specifies how a deposit account holder may submit a payment to the Office to replenish the deposit account. A payment to replenish a deposit account may be submitted by:

- (A) making the payment by electronic funds transfer through the Federal Reserve Fedwire System. Deposit account holders who use the Federal Reserve Fedwire System must provide the following information to their bank or financial institution: (1) Name of the Bank, which is Treas NYC (Treasury New York City); (2) Bank Routing Code, which is 021030004; (3) United States Patent and Trademark Office account number with the Department of Treasury, which is 13100001; and (4) the deposit account holder’s company name and deposit account number. The deposit account holder should inform his or her bank or financial institution to use due care to ensure that all pertinent account numbers are listed on the transaction because the failure to include the proper deposit account number will delay the processing of the replenishment;

- (B) electronic funds transfer over the Office’s Internet website (www.uspto.gov); or

- (C) mailing the payment to: Mail Stop Deposit Accounts, Director of the United States Patent and Trademark Office, P.O. Box 1450, Alexandria, Virginia 22313-1450.

For deposit account replenishments to be delivered by mail to the USPTO by a delivery service (e.g., Federal Express (FedEx), UPS, DHL, Laser, Action, Purolator, etc.), rather than by the United States Postal Service (USPS), the deposit account replenishments should be addressed to the Customer Service Window (see MPEP § 501, subsection III) with “Mail Stop Deposit Accounts” included in the address.

In the event a payment to replenish a deposit account is refused (e.g., for insufficient funds or due to a stop payment order), the fee under 37 CFR 1.21(m) for processing the payment refusal will be charged to the deposit account. Further information on deposit account replenishment may be obtained from the Office’s Internet website or by contacting the Deposit Account Division at (571) 272-6500.

III. REFUNDS TO A DEPOSIT ACCOUNTFor refunds to a deposit account, see MPEP § 607.02.

509.02 Small Entity Status — Definitions [R-01.2024]

Under 35 U.S.C. 41(h)(1), fees charged under 35 U.S.C. 41(a), (b) and (d)(1) shall be reduced by 60 percent with respect to their application to any small business concern as defined under section 3 of the Small Business Act, and to any independent inventor or nonprofit organization as defined in regulations issued by the Director. Effective March 19, 2013, the availability of the small entity discount was extended to certain other fees not contained in 35 U.S.C. 41(a), (b) and (d)(1), but which are included among fees “for filing, searching, examining, issuing, appealing, and maintaining patent applications and patents” as authorized by the Leahy-Smith America Invents Act (AIA), Public Law 112-29, sec. 10(b), 125 Stat. 284 (September 16, 2011). Effective January 1, 2014, the small entity discount also became available to certain “filing, searching, [and] examining” fees for international applications under the Patent Cooperation Treaty (PCT). Effective December 29, 2022, the small entity discount was increased from 50 percent to 60 percent for most fees by the Unleashing American Innovators Act of 2022, Public Law 117-328, division W, sec. 107, 136 Stat. 4459 (December 29, 2022). Note that if applicant qualifies as a small entity under 37 CFR 1.27, applicant may also qualify for “Micro Entity Status” under 35 U.S.C. 123. See 37 CFR 1.29 and MPEP § 509.04et seq. for the requirements to establish micro entity status for the purpose of paying micro entity fees.

As of December 29. 2022, the following fees are reduced by 60 percent for small entities: patent application filing fees including the basic filing fee, search fee, examination fee, application size fee, and excess claims fees (37 CFR 1.16); extension of time fees, revival fees, certain petition fees, and the fee for submitting an information disclosure statement in certain time frames (37 CFR 1.17); patent issue fees (37 CFR 1.18); maintenance fees on patents and request for reexamination fees (37 CFR 1.20); and appeals fees (37 CFR 41.20). The increase in the small entity discount for the search fee and the supplemental search fee for international applications under the PCT applies to applications having a receipt date on or after April 1, 2023 (37 CFR 1.445(a)(2) and (a)(3)). Additionally, the increase in the small entity discount for the late furnishing of a sequence listing fee (37 CFR 1.445(a)(5)) and the international preliminary examination and processing fees for international applications under the PCT (37 CFR 1.482(a)) became effective on April 1, 2023. The increase in the small entity discount fee for international design applications under the Hague Agreement applies to applications having a date of international registration on or after May 1, 2023 (37 CFR 1.18(b)(1)).

Fees which are not reduced include document supply fees (37 CFR 1.19), certificate of correction fees (37 CFR 1.20(a)), and most miscellaneous fees and charges (37 CFR 1.21), fees for lengthy sequence listings under 37 CFR 1.21(o) are reduced. There is only one fee for which a small entity discount was offered prior to March 19, 2013 that is now ineligible for a small entity discount – the fee for a statutory disclaimer under 37 CFR 1.20(d).

The Consolidated Appropriations Act, 2005, provides that the filing fee charged under 35 U.S.C. 41(a)(1)(A) shall be reduced by 75 percent with respect to its application to any small entity "if the application is filed by electronic means as prescribed by the Director" (35 U.S.C. 41(h)(3)). This fee reduction was increased to 80 percent in the Unleashing American Innovators Act of 2022. Therefore, the filing fee for a nonprovisional original utility application filed on or after December 29, 2022 by a small entity in compliance with the USPTO patent electronic filing system is reduced by 80 percent. See 37 CFR 1.16(a). The 80 percent reduction set forth in 35 U.S.C. 41(h)(3) does not apply to design applications, plant applications, reissue applications, or provisional applications.

35 U.S.C. 41(h)(1) gives the Director the authority to establish regulations defining independent inventors and nonprofit organizations. The Small Business Administration was given authority to establish the definition of a small business concern. A small entity for purposes of paying reduced fees is defined in 37 CFR 1.27(a) as a person, a small business concern, or a nonprofit organization. The term “person” rather than “independent inventor” is used since individuals who are not inventors but who have received some rights in the invention are intended to be covered by 37 CFR 1.27.

37 CFR 1.27 Definition of small entities and establishing status as a small entity to permit payment of small entity fees; when a determination of entitlement to small entity status and notification of loss of entitlement to small entity status are required; fraud on the Office.

- (a) Definition of small entities. A small entity as used in this

chapter means any party (person, small business concern, or nonprofit

organization) under paragraphs (a)(1) through (a)(3) of this section.

- (1) Person. A person, as used in paragraph (c) of this section, means any inventor or other individual (e.g., an individual to whom an inventor has transferred some rights in the invention) who has not assigned, granted, conveyed, or licensed, and is under no obligation under contract or law to assign, grant, convey, or license, any rights in the invention. An inventor or other individual who has transferred some rights in the invention to one or more parties, or is under an obligation to transfer some rights in the invention to one or more parties, can also qualify for small entity status if all the parties who have had rights in the invention transferred to them also qualify for small entity status either as a person, small business concern, or nonprofit organization under this section.

- (2) Small business concern. A small business concern, as

used in paragraph (c) of this section, means any business concern

that:

- (i) Has not assigned, granted, conveyed, or licensed, and is under no obligation under contract or law to assign, grant, convey, or license, any rights in the invention to any person, concern, or organization which would not qualify for small entity status as a person, small business concern, or nonprofit organization; and

- (ii) Meets the size standards set forth in 13 CFR 121.801 through 121.805 to be eligible for reduced patent fees. Questions related to standards for a small business concern may be directed to: Small Business Administration, Size Standards Staff, 409 Third Street, SW., Washington, DC 20416.

- (3) Nonprofit Organization. A nonprofit organization, as

used in paragraph (c) of this section, means any nonprofit organization

that:

- (i) Has not assigned, granted, conveyed, or licensed, and is under no obligation under contract or law to assign, grant, convey, or license, any rights in the invention to any person, concern, or organization which would not qualify as a person, small business concern, or a nonprofit organization; and

- (ii) Is either:

- (A) A university or other institution of higher education located in any country;

- (B) An organization of the type described in section 501(c)(3) of the Internal Revenue Code of 19 86 (26 U.S.C. 501(c)(3)) and exempt from taxation under section 501(a) of the Internal Revenue Code (26 U.S.C. 501(a));

- (C) Any nonprofit scientific or educational organization qualified under a nonprofit organization statute of a state of this country (35 U.S.C. 201(i)); or

- (D) Any nonprofit organization located in a foreign country which would qualify as a nonprofit organization under paragraphs (a)(3)(ii)(B) of this section or (a)(3)(ii)(C) of this section if it were located in this country.

- (4) Federal Government Use License Exceptions. In a patent

application filed, prosecuted, and if patented, maintained at no expense

to the Government, with the exception of any expense taken to deliver the

application and fees to the Office on behalf of the applicant:

- (i) For persons under paragraph (a)(1)

of this section, claiming small entity status is not prohibited

by:

- (A) A use license to the Government resulting from a rights determination under Executive Order 10096 made in accordance with §501.60 of this title;

- (B) A use license to the Government resulting from Federal agency action pursuant to 15 U.S.C. 3710d(a) allowing the Federal employee-inventor to obtain or retain title to the invention; or

- (C) A use license to a Federal agency resulting from retention of rights under 35 U.S.C. 202(d) by an inventor employed by a small business concern or nonprofit organization contractor, provided the license is equivalent to the license under 35 U.S.C. 202(c)(4) the Federal agency would have received had the contractor elected to retain title, and all the conditions applicable under § 401.9 of this title to an employee/ inventor are met.

- (ii) For small business concerns and

nonprofit organizations under paragraphs (a)(2) and (3) of this

section, a use license to a Federal agency resulting from a funding

agreement with that agency pursuant to 35 U.S.C.

202(c)(4) does not preclude claiming small

entity status, provided that:.

- (A) The subject invention was made solely by employees of the small business concern or nonprofit organization; or

- (B) In the case of a Federal employee co-inventor, the Federal agency employing such co-inventor took action pursuant to 35 U.S.C. 202(e)(1) to exclusively license or assign whatever rights currently held or that it may acquire in the subject invention to the small business concern or nonprofit organization, subject to the license under 35 U.S.C. 202(c)(4).

- (iii) For small business concerns and

nonprofit organizations under paragraphs (a)(2) and (3) of this

section that have collaborated with a Federal agency laboratory

pursuant to a cooperative research and development agreement

(CRADA) under 15 U.S.C. 3710a(a)(1), claiming small entity status

is not prohibited by a use license to the Government pursuant

to:

- (A) 15 U.S.C. 3710a(b)(2) that results from retaining title to an invention made solely by the employee of the small business concern or nonprofit organization; or

- (B) 15 U.S.C. 3710a(b)(3)(D), provided the laboratory has waived in whole any right of ownership the Government may have to the subject invention made by the small business concern or nonprofit organization, or has exclusively licensed whatever ownership rights the Government may acquire in the subject invention to the small business concern or nonprofit organization.

- (iv) ) Regardless of whether an exception under this paragraph (a)(4) applies, no refund under § 1.28(a) is available for any patent fee paid by the Government.

- (i) For persons under paragraph (a)(1)

of this section, claiming small entity status is not prohibited

by:

- (5) Security Interest. A security interest does not involve an obligation to transfer rights in the invention for the purposes of paragraphs (a)(1) through (a)(3) of this section unless the security interest is defaulted upon.

*****

37 CFR 1.27(a)(1) defines a person as any inventor or other individual (e.g., an individual to whom an inventor has transferred some rights in the invention), who has not assigned, granted, conveyed, or licensed, and is under no obligation under contract or law to assign, grant, convey, or license, any rights in the invention. An inventor or other individual who has transferred some rights, or is under an obligation to transfer some rights in the invention to one or more parties, can also qualify for small entity status if all the parties who have had rights in the invention transferred to them also qualify for small entity status either as a person, small business concern, or nonprofit organization.

II. SMALL BUSINESS CONCERNIn order to be eligible for reduced patent fees as a “small business concern” under 37 CFR 1.27(a)(2), a business concern must meet the standards set forth in 13 CFR 121.801 through 121.805. Questions relating to standards for a small business concern may be directed to:

Small Business Administration

Office of Size Standards

409 Third Street, S.W.

Washington, DC 20416

(202)205-6618

Email: sizestandards@sba.gov

37 CFR 1.27(a)(3) defines a nonprofit organization by utilizing and interpreting the definition contained in 35 U.S.C. 201(i). The term “university or other institution of higher education” as used in 37 CFR 1.27(a)(3)(ii)(A) means an educational institution which

- (A) admits as regular students only persons having a certificate of graduation from a school providing secondary education, or the recognized equivalent of such a certificate,

- (B) is legally authorized within the jurisdiction in which it operates to provide a program of education beyond secondary education,

- (C) provides an educational program for which it awards a bachelor’s degree or provides not less than a 2-year program which is acceptable for full credit toward such a degree,

- (D) is a public or other nonprofit institution, and

- (E) is accredited by a nationally recognized accrediting agency or association, or if not so accredited, is an institution that has been granted preaccreditation status by such agency or association that has been recognized by the Secretary for the granting of preaccreditation status, and the Secretary has determined that there is satisfactory assurance that the institution will meet the accreditation standards of such an agency or association within a reasonable time.

The definition of “university or other institution of higher education” as set forth herein essentially follows the definition of “institution of higher education” contained in 20 U.S.C. 1000. Institutions which are strictly research facilities, manufacturing facilities, service organizations, etc., are not intended to be included within the term “other institution of higher education” even though such institutions may perform an educational function or publish the results of their work.

Nonprofit organizations also include organizations of the type described in section 501(c)(3) of the Internal Revenue Code of 1986 (26 U.S.C. 501(c)(3)) and which are exempt from taxation under 26 U.S.C. 501(a). Organizations described in 26 U.S.C. 501(c)(3) include corporations, and any community chest, fund, or foundation, organized and operated exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster national or international amateur sports competition (but only if no part of its activities involve the provision of athletic facilities or equipment), or for the prevention of cruelty to children or animals, no part of the net earnings of which inures to the benefit of any private shareholder or individual, no substantial part of the activities of which is carrying on propaganda, or otherwise attempting to influence legislation (limited exceptions may apply under 26 U.S.C. 501(h)) and which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public office.

IV. LOCATION OF SMALL ENTITYSmall entities may claim reduced fees regardless of the country in which they are located. There is no restriction requiring that the person, small business concern, or nonprofit organization be located in the United States. The same definitions apply to all applicants equally in accordance with the Paris Convention for the Protection of Industrial Property.

V. RIGHTS IN THE INVENTION AND TRANSFER OF RIGHTSThe “rights in the invention” under 37 CFR 1.27(a)(1), (a)(2)(i), and (a)(3)(i) are the rights in the United States. Rights in the invention include the right to exclude others from making, using, offering for sale, or selling the invention throughout the United States or importing the invention into the United States. Therefore, for example, status as a small entity is lost by an inventor who has transferred or has an obligation to transfer a shop right to an employer who could not qualify as a small entity.

Individual inventors (37 CFR 1.27(a)(1)), small business concerns (37 CFR 1.27(a)(2)), and nonprofit organizations (37 CFR 1.27(a)(3)) can make an assignment, grant, conveyance, or license of partial rights in the invention to another individual(s), small business concern, or nonprofit organization who could qualify as a person (37 CFR 1.27(a)(1)), small business concern, or nonprofit organization. Under the circumstances described, the individual inventor, small business concern, or nonprofit organization could still qualify for small entity status. However, if the individual inventor, small business concern, or nonprofit organization assigned, granted, conveyed, or licensed, or came under an obligation to assign, grant, convey, or license, any rights to the invention to any individual, small business concern, or nonprofit organization which would not qualify as a small entity (37 CFR 1.27(a)), then the inventor, small business concern, or nonprofit organization would no longer qualify for small entity status.

With regard to transfer of rights in the invention, the rights in question are those in the United States to be covered by an application or patent. Transfer of rights to a Japanese patent, for example, would not affect small entity status if no rights in the United States to a corresponding patent were likewise transferred.

The payment of reduced fees under 35 U.S.C. 41 is limited to those situations in which all of the rights in the invention are owned by small entities, i.e., persons, small business concerns, or nonprofit organizations. To do otherwise would be clearly contrary to the intended purpose of the legislation which contains no indication that fees are to be reduced in circumstances where rights are owned by non-small entities. For example, a non-small entity is not permitted to transfer patent rights to a small business concern which would pay the reduced fees and grant a license to the entity.

If rights transferred to a non-small entity are later returned to a small entity so that all rights are held by small entities, reduced fees may be claimed.

The term “license” in the definitions includes nonexclusive as well as exclusive licenses and royalty free as well as royalty generating licenses. Implied licenses to use and resell patented articles purchased from a small entity, however, will not preclude the proper claiming of small entity status. Likewise, an order by an applicant to a firm to build a prototype machine or product for the applicant’s own use is not considered to constitute a license for purposes of the definitions. A grant of a non-exclusive license to a non-small entity will disqualify applicant from claiming small entity status. See Ulead Systems, Inc. v. Lex Computer & Management Corp., 351 F.3d 1139, 1142, 69 USPQ2d 1097, 1099 (Fed. Cir. 2003).

A security interest does not involve an obligation to transfer rights in the invention for the purposes of 37 CFR 1.27(a)(1) through (a)(3) unless the security interest is defaulted upon. See 37 CFR 1.27(a)(5). For example, an applicant or patentee may take out a loan from a large entity banking institution and the loan may be secured with rights in a patent application or patent of the applicant or patentee, respectively. The granting of such a security interest to the banking institution is not a currently enforceable obligation to assign, grant, convey, or license any rights in the invention to the banking institution. Only if the loan is defaulted upon will the security interest permit a transfer of rights in the application or patent to the banking institution. Thus, where the banking institution is a large entity, the applicant or patentee would not be prohibited from claiming small entity status merely because the banking institution has been granted a security interest, but if the loan is defaulted upon, there would be a loss of entitlement to small entity status. Pursuant to 37 CFR 1.27(g), notification of the loss of entitlement due to default on the terms of the security interest would need to be filed in the application or patent prior to paying, or at the time of paying, the earliest of the issue fee or any maintenance fee due after the date on which small entity status is no longer appropriate. See MPEP § 509.03(b), subsection I.

Once small entity status is established in an application or patent, fees as a small entity may thereafter be paid in that application or patent without regard to a change in status until the issue fee is due or any maintenance fee is due. 37 CFR 1.27(g)(1). 37 CFR 1.27(g)(2) requires that notification of any change in status resulting in loss of entitlement to small entity status be filed in the application or patent prior to paying, or at the time of paying, the earliest of the issue fee or any maintenance fee due after the date on which status as a small entity is no longer appropriate. 37 CFR 1.27(g)(2) also requires that the notification of loss of entitlement to small entity status be in the form of a specific written assertion to that extent, rather than only payment of a non-small entity fee. For example, when paying the issue fee in an application that has previously been accorded small entity status and the required new determination of continued entitlement to small entity status reveals that status has been lost, applicant should not just simply pay the non-small entity issue fee or cross out the recitation of small entity status on Part B of the Notice of Allowance and Fee(s) Due (PTOL-85), but should (A) check the appropriate box on Part B of the PTOL-85 form to indicate that there has been a change in entity status and applicant is no longer claiming small entity status, and (B) pay the fee amount for a non-small entity.

VI. RIGHTS HELD BY GOVERNMENT ORGANIZATIONSAlthough the Federal government agencies do not qualify as nonprofit organizations for paying reduced fees under the rules, a license to a Federal agency resulting from a funding agreement with the agency pursuant to 35 U.S.C. 202(c)(4) will not preclude the proper claiming of small entity status. See 37 CFR 1.27(a)(4)(ii), which provides that:

“For small business concerns and nonprofit organizations under paragraphs (a)(2) and (3) of this section, a use license to a Federal agency resulting from a funding agreement with that agency pursuant to 35 U.S.C. 202(c)(4) does not preclude claiming small entity status, provided that:

- (A) The subject invention was made solely by employees of the small business concern or nonprofit organization; or

- (B) In the case of a Federal employee co-inventor, the Federal agency employing such co-inventor took action pursuant to 35 U.S.C. 202(e)(1) to exclusively license or assign whatever rights currently held or that it may acquire in the subject invention to the small business concern or nonprofit organization, subject to the license under 35 U.S.C. 202(c)(4).”

In addition, regarding a government use license arising from an obligation under a cooperative research and development agreement (CRADA) with a Federal Agency pursuant to 15 U.S.C. 3710a(b), 37 CFR 1.27(a)(4)(iii) provides that:

“For small business concerns and nonprofit organizations under paragraphs (a)(2) and (3) of this section that have collaborated with a Federal agency laboratory pursuant to a cooperative research and development agreement (CRADA) under 15 U.S.C. 3710a(a)(1), claiming small entity status is not prohibited by a use license to the Government pursuant to:

- (A) (A) 15 U.S.C. 3710a(b)(2) that results from retaining title to an invention made solely by the employee of the small business concern or nonprofit organization; or

- (B) (B) 15 U.S.C. 3710a(b)(3)(D), provided the laboratory has waived in whole any right of ownership the Government may have to the subject invention made by the small business concern or nonprofit organization, or has exclusively licensed whatever ownership rights the Government may acquire in the subject invention to the small business concern or nonprofit organization.”

Furthermore, as provided in 37 CFR 1.27(a)(4)(i), the following situations do not constitute a license so as to prohibit claiming small entity status by a person under 37 CFR 1.27(a)(1):

- 1. a use license to the Government resulting from a rights determination under Executive Order 10096 , made in accordance with 35 U.S.C. 501.6;

- 2. a use license to the Government resulting from Federal agency action pursuant to 15 U.S.C. 3710d(a) allowing the Federal employee inventor to obtain or retain title to the invention; or

- 3. a use license to a Federal agency resulting from retention of rights by the inventor under 35 U.S.C. 202(d), provided the conditions under 35 U.S.C. 401.9 for retention of rights by an inventor employed by a small business concern or nonprofit organization contractor are met, and the license is equivalent to the license the Federal agency would have received had the contractor elected to retain title

Government organizations as such, whether domestic or foreign, cannot qualify as nonprofit organizations as defined in 37 CFR 1.27(a)(3). Thus, for example, a government research facility or other government-owned corporation could not qualify. 37 CFR 1.27(a)(3) was based upon 35 U.S.C. 201(i), as established by Public Law 96-517. The limitation to “an organization of the type described in section 501(c)(3) of the Internal Revenue Code of 1986 (26 U.S.C. 501(c)(3)) and exempt from taxation under section 501(a) of the Internal Revenue Code (26 U.S.C. 501(a))” would by its nature exclude the U.S. government and its agencies and facilities, including research facilities and government corporations. State and foreign governments and governmental agencies and facilities would be similarly excluded. 37 CFR 1.27(a)(3) is not intended to include within the definition of a nonprofit organization government organizations of any kind located in any country. A university or other institution of higher education located in any country would qualify, however, as a “nonprofit organization” under 37 CFR 1.27(a)(3) even though it has some government affiliation since such institutions are specifically included.

A wholly owned subsidiary of a nonprofit organization or of a university is considered a part of the nonprofit organization or university and is not precluded from qualifying for small entity status.

509.03 Claiming Small Entity Status [R-01.2024]

37 CFR 1.27 Definition of small entities and establishing status as a small entity to permit payment of small entity fees; when a determination of entitlement to small entity status and notification of loss of entitlement to small entity status are required; fraud on the Office.

*****

- (b) Establishment of small entity status permits payment of reduced

fees.

- (1) A small entity, as defined in paragraph (a) of this section, who has properly asserted entitlement to small entity status pursuant to paragraph (c) of this section will be accorded small entity status by the Office in the particular application or patent in which entitlement to small entity status was asserted. Establishment of small entity status allows the payment of certain reduced patent fees pursuant to 35 U.S.C. 41(h)(1).

- (2) Submission of an original utility application in compliance with the USPTO patent electronic filing system by an applicant who has properly asserted entitlement to small entity status pursuant to paragraph (c) of this section in that application allows the payment of a reduced filing fee pursuant to 35 U.S.C. 41(h)(3).

- (c) Assertion of small entity status. Any party (person, small

business concern or nonprofit organization) should make a determination,

pursuant to paragraph (f) of this section, of entitlement to be accorded small

entity status based on the definitions set forth in paragraph (a) of this

section, and must, in order to establish small entity status for the purpose of

paying small entity fees, actually make an assertion of entitlement to small

entity status, in the manner set forth in paragraphs (c)(1) or (c)(3) of this

section, in the application or patent in which such small entity fees are to be

paid.

- (1) Assertion by writing. Small entity status

may be established by a written assertion of entitlement to small entity

status. A written assertion must:

- (i) Be clearly identifiable;

- (ii) Be signed (see paragraph (c)(2) of this section); and

- (iii) Convey the concept of entitlement to small entity status, such as by stating that applicant is a small entity, or that small entity status is entitled to be asserted for the application or patent. While no specific words or wording are required to assert small entity status, the intent to assert small entity status must be clearly indicated in order to comply with the assertion requirement.

- (1) Assertion by writing. Small entity status

may be established by a written assertion of entitlement to small entity

status. A written assertion must:

*****

-

-

- (3) Assertion by payment of the small entity basic filing,

basic transmittal, basic national fee, international search fee,

or individual designation fee in an international design

application. The payment, by any party, of the exact

amount of one of the small entity basic filing fees set forth in

§ 1.16(a), (b), (c), (d), or

(e), the small entity transmittal fee set

forth in§ 1.445(a)(1)

or § 1.1031(a),

the small entity international search fee set forth in

§ 1.445(a)(2)

to a Receiving Office other than the United States Receiving Office

in the exact amount established for that Receiving Office pursuant

toPCT Rule 16, or

the small entity basic national fee set forth in §

1.492(a), will be treated as a written

assertion of entitlement to small entity status even if the type of

basic filing, basic transmittal, or basic national fee is

inadvertently selected in error. The payment, by any party, of the

small entity first part of the individual designation fee for the

United States to the International Bureau (§

1.1031) will be treated as a written

assertion of entitlement to small entity status.

- (i) If the Office accords small entity status based on payment of a small entity basic filing or basic national fee under paragraph (c)(3) of this section that is not applicable to that application, any balance of the small entity fee that is applicable to that application will be due along with the appropriate surcharge set forth in § 1.16(f), or § 1.16(g).

- (ii) The payment of any small entity fee other than those set forth in paragraph (c)(3) of this section (whether in the exact fee amount or not) will not be treated as a written assertion of entitlement to small entity status and will not be sufficient to establish small entity status in an application or a patent.

- (4) Assertion required in related, continuing, and reissue applications. Status as a small entity must be specifically established by an assertion in each related, continuing and reissue application in which status is appropriate and desired. Status as a small entity in one application or patent does not affect the status of any other application or patent, regardless of the relationship of the applications or patents. The refiling of an application under § 1.53 as a continuation, divisional, or continuation-in-part application (including a continued prosecution application under § 1.53(d)), or the filing of a reissue application, requires a new assertion as to continued entitlement to small entity status for the continuing or reissue application.

- (3) Assertion by payment of the small entity basic filing,

basic transmittal, basic national fee, international search fee,

or individual designation fee in an international design

application. The payment, by any party, of the exact

amount of one of the small entity basic filing fees set forth in

§ 1.16(a), (b), (c), (d), or

(e), the small entity transmittal fee set

forth in§ 1.445(a)(1)

or § 1.1031(a),

the small entity international search fee set forth in

§ 1.445(a)(2)

to a Receiving Office other than the United States Receiving Office

in the exact amount established for that Receiving Office pursuant

toPCT Rule 16, or

the small entity basic national fee set forth in §

1.492(a), will be treated as a written

assertion of entitlement to small entity status even if the type of

basic filing, basic transmittal, or basic national fee is

inadvertently selected in error. The payment, by any party, of the

small entity first part of the individual designation fee for the

United States to the International Bureau (§

1.1031) will be treated as a written

assertion of entitlement to small entity status.

-

- (d) When small entity fees can be paid. Any fee, other than the small entity basic filing fees and the small entity national fees of paragraph (c)(3) of this section, can be paid in the small entity amount only if it is submitted with, or subsequent to, the submission of a written assertion of entitlement to small entity status, except when refunds are permitted by § 1.28(a).

- (e) Only one assertion required.

- (1) An assertion of small entity status need only be filed once in an application or patent. Small entity status, once established, remains in effect until changed pursuant to paragraph (g)(1) of this section. Where an assignment of rights or an obligation to assign rights to other parties who are small entities occurs subsequent to an assertion of small entity status, a second assertion is not required.

- (2) Once small entity status is withdrawn pursuant to paragraph (g)(2) of this section, a new written assertion is required to again obtain small entity status.

- (f) Assertion requires a determination of entitlement to pay small entity fees. Prior to submitting an assertion of entitlement to small entity status in an application, including a related, continuing, or reissue application, a determination of such entitlement should be made pursuant to the requirements of paragraph (a) of this section. It should be determined that all parties holding rights in the invention qualify for small entity status. The Office will generally not question any assertion of small entity status that is made in accordance with the requirements of this section, but note paragraph (h) of this section.

- (g)

- (1) New determination of entitlement to small entity status is needed when issue and maintenance fees are due. Once status as a small entity has been established in an application or patent, fees as a small entity may thereafter be paid in that application or patent without regard to a change in status until the issue fee is due or any maintenance fee is due.

- (2) Notification of loss of entitlement to small entity status is required when issue and maintenance fees are due. Notification of a loss of entitlement to small entity status must be filed in the application or patent prior to paying, or at the time of paying, the earliest of the issue fee or any maintenance fee due after the date on which status as a small entity as defined in paragraph (a) of this section is no longer appropriate. The notification that small entity status is no longer appropriate must be signed by a party identified in § 1.33(b). Payment of a fee in other than the small entity amount is not sufficient notification that small entity status is no longer appropriate.

- (h) Fraud attempted or practiced on the Office.

- (1) Any attempt to fraudulently establish status as a small entity, or pay fees as a small entity, shall be considered as a fraud practiced or attempted on the Office.

- (2) Improperly, and with intent to deceive, establishing status as a small entity, or paying fees as a small entity, shall be considered as a fraud practiced or attempted on the Office.

37 CFR 1.4 Nature of correspondence and signature requirements.

*****

- (d)

- *****

- (4) Certifications.

- (i) Certification as to the paper presented. The presentation to the Office (whether by signing, filing, submitting, or later advocating) of any paper by a party, whether a practitioner or non-practitioner, constitutes a certification under § 11.18(b) of this subchapter. Violations of § 11.18(b)(2) of this subchapter by a party, whether a practitioner or non-practitioner, may result in the imposition of sanctions under § 11.18(c) of this subchapter. Any practitioner violating § 11.18(b) of this subchapter may also be subject to disciplinary action. See § 11.18(d) of this subchapter.

- (ii) Certification as to the signature. The person inserting a signature under paragraph (d)(2) or (d)(3) of this section in a document submitted to the Office certifies that the inserted signature appearing in the document is his or her own signature. A person submitting a document signed by another under paragraph (d)(2) or (d)(3) of this section is obligated to have a reasonable basis to believe that the person whose signature is present on the document was actually inserted by that person, and should retain evidence of authenticity of the signature. Violations of the certification as to the signature of another or a person’s own signature as set forth in this paragraph may result in the imposition of sanctions under § 11.18(c) and (d) of this chapter.

*****

37 CFR 11.18 Signature and certificate for correspondence filed in the Office.

*****

- (b) By presenting to the Office or hearing officer in a

disciplinary proceeding (whether by signing, filing, submitting, or later

advocating) any paper, the party presenting such paper, whether a practitioner

or non-practitioner, is certifying that—

- (1) All statements made therein of the party’s own knowledge are true, all statements made therein on information and belief are believed to be true, and all statements made therein are made with the knowledge that whoever, in any matter within the jurisdiction of the Office, knowingly and willfully falsifies, conceals, or covers up by any trick, scheme, or device a material fact, or knowingly and willfully makes any false, fictitious, or fraudulent statements or representations, or knowingly and willfully makes or uses any false writing or document knowing the same to contain any false, fictitious, or fraudulent statement or entry, shall be subject to the penalties set forth under 18 U.S.C. 1001 and any other applicable criminal statute, and violations of the provisions of this section may jeopardize the probative value of the paper; and

- (2) To the best of the party’s knowledge, information and

belief, formed after an inquiry reasonable under the circumstances,

- (i) The paper is not being presented for any improper purpose, such as to harass someone or to cause unnecessary delay or needless increase in the cost of any proceeding before the Office;

- (ii) The other legal contentions therein are warranted by existing law or by a nonfrivolous argument for the extension, modification, or reversal of existing law or the establishment of new law;

- (iii) The allegations and other factual contentions have evidentiary support or, if specifically so identified, are likely to have evidentiary support after a reasonable opportunity for further investigation or discovery; and

- (iv) The denials of factual contentions are warranted on the evidence, or if specifically so identified, are reasonably based on a lack of information or belief.

*****

In order to establish small entity status for the purpose of paying small entity fees, any party (person, small business concern or nonprofit organization) must make an assertion of entitlement to small entity status in the manner set forth in 37 CFR 1.27(c)(1) or (c)(3), in the application or patent in which such small entity fees are to be paid. Under 37 CFR 1.27, as long as all of the rights remain in small entities, the fees established for a small entity can be paid. This includes circumstances where the rights were divided between a person, a small business concern, and a nonprofit organization, or any combination thereof.

Under 37 CFR 1.4(d)(4), an assertion of entitlement to small entity status, including the mere payment of an exact small entity basic filing fee, inherently contains a certification under 37 CFR 11.18(b). It is not required that an assertion of entitlement to small entity status be filed with each fee paid. Rather, once status as a small entity has been established in an application or patent, fees as a small entity may thereafter be paid in that application or patent without regard to a change in status until the issue fee is due or any maintenance fee is due. 37 CFR 1.27(g)(1). Notification of a loss of entitlement to small entity status must be filed in the application or patent prior to paying, or at the time of paying, the earliest of the issue fee or any maintenance fee due after the date on which status as a small entity is no longer appropriate. 37 CFR 1.27(g)(2).

Status as a small entity may be established in a provisional application by complying with 37 CFR 1.27.

Status as a small entity must be specifically established in each application or patent in which the status is available and desired. Status as a small entity in one application or patent does not affect any other application or patent, including applications or patents which are directly or indirectly dependent upon the application or patent in which the status has been established. The filing of an application under 37 CFR 1.53 as a continuation-in-part, continuation or division (including a continued prosecution application under 37 CFR 1.53(d) for design applications), or the filing of a reissue application requires a new assertion as to continued entitlement to small entity status for the continuing or reissue application. Submission of a request for continued examination (RCE) under 37 CFR 1.114 does not require a new determination or assertion of entitlement to small entity status since it is not a new application.

Examiners may use the following form paragraph to notify applicant that they may qualify for small entity status.

¶ 5.05 Small Entity Status

This application may qualify for “Small Entity Status” and, therefore, applicant may be entitled to the payment of reduced fees. In order to establish small entity status for the purpose of paying small entity fees, applicant must make a determination of entitlement to small entity status under 37 CFR 1.27(f) and make an assertion of entitlement to small entity status in the manner set forth in 37 CFR 1.27(c)(1) or 37 CFR 1.27(c)(3). Accordingly, if applicant meets the requirements of 37 CFR 1.27(a), applicant must submit a written assertion of entitlement to small entity status under 37 CFR 1.27(c) before fees can be paid in the small entity amount. See 37 CFR 1.27(d). The assertion must be signed, clearly identifiable, and convey the concept of entitlement to small entity status. See 37 CFR 1.27(c)(1). No particular form is required. If applicant qualifies as a small entity under 37 CFR 1.27, applicant may also qualify for “Micro Entity Status” under 35 U.S.C. 123. See 37 CFR 1.29 for the requirements to establish micro entity status for the purpose of paying micro entity fees.

Small entity status may be established by the submission of a simple written assertion of entitlement to small entity status. The assertion must be signed, clearly identifiable, and convey the concept of entitlement to small entity status. 37 CFR 1.27(c)(1). The written assertion is not required to be presented in any particular form. Written assertions of small entity status or references to small entity fees will be liberally interpreted to represent the required assertion. The written assertion can be made in any paper filed in or with the application and need be no more than a simple sentence or a box checked on an application transmittal letter.

II. PARTIES WHO CAN ASSERT AND SIGN AN ENTITLEMENT TO SMALL ENTITY STATUS BY WRITINGA. Applications Filed On or After September 16, 201237 CFR 1.27 Definition of small entities and establishing status as a small entity to permit payment of small entity fees; when a determination of entitlement to small entity status and notification of loss of entitlement to small entity status are required; fraud on the Office.

*****

- (c) Assertion of small entity status. Any party

(person, small business concern or nonprofit organization) should make a

determination, pursuant to paragraph (f) of this section, of entitlement

to be accorded small entity status based on the definitions set forth in

paragraph (a) of this section, and must, in order to establish small

entity status for the purpose of paying small entity fees, actually make

an assertion of entitlement to small entity status, in the manner set

forth in paragraphs (c)(1) or (c)(3) of this section, in the application

or patent in which such small entity fees are to be paid.

- (1) Assertion by writing. Small entity

status may be established by a written assertion of entitlement to

small entity status. A written assertion must:

- (i) Be clearly identifiable;

- (ii) Be signed (see paragraph (c)(2) of this section); and

- (iii) Convey the concept of entitlement to small entity status, such as by stating that applicant is a small entity, or that small entity status is entitled to be asserted for the application or patent. While no specific words or wording are required to assert small entity status, the intent to assert small entity status must be clearly indicated in order to comply with the assertion requirement.

- (2) Parties who can sign and file the written assertion. The written assertion can be signed by:

- (3) Assertion by payment of the small entity basic filing,

basic transmittal, basic national fee, or international search

fee, or individual designation fee in an international design

application. The payment, by any party, of the exact

amount of one of the small entity basic filing fees set forth in

§§ 1.16(a),

1.16(b),

1.16(c),

1.16(d),

1.16(e), the

small entity transmittal fee set forth in §

1.445(a)(1), the small entity international

search fee set forth in § 1.445(a)(2)

to a Receiving Office other than the United States Receiving Office

in the exact amount established for that Receiving Office pursuant

to PCT Rule 16, or

the small entity basic national fee set forth in §

1.492(a), will be treated as a written

assertion of entitlement to small entity status even if the type of

basic filing, basic transmittal, or basic national fee is

inadvertently selected in error. The payment, by any party, of the

small entity first part of the individual designation fee for the

United States to the International Bureau (§

1.1031) will be treated as a written

assertion of entitlement to small entity status.

- (i) If the Office accords small entity status based on payment of a small entity basic filing or basic national fee under paragraph (c)(3) of this section that is not applicable to that application, any balance of the small entity fee that is applicable to that application will be due along with the appropriate surcharge set forth in § 1.16(f), or § 1.16(g).

- (ii) The payment of any small entity fee other than those set forth in paragraph (c)(3) of this section (whether in the exact fee amount or not) will not be treated as a written assertion of entitlement to small entity status and will not be sufficient to establish small entity status in an application or a patent.

- (1) Assertion by writing. Small entity

status may be established by a written assertion of entitlement to

small entity status. A written assertion must:

*****