Select from the following for more information on this page

Subject matter descriptions Highlights Prior partnership meetings Statistics Guidance and training materials Outreach opportunities and presentations Examiner decision making process Contact us

The Business Methods area of the USPTO is a collection of subject matter areas in Technology Center 3600 that grants patents related to Data Processing: Financial, Business Practice, Management, or Cost/Pricing Determination. A Business Method patent is a utility patent that protects a method of doing business. The 3620 and the 3680 workgroups examine applications pertaining to advertising, incentive programs, and coupons; cost/price, reservations, shipping, and transportation; cryptography and business data security; electronic shopping; healthcare; inventory, point of sale, and accounting; miscellaneous; and operations research. The 3690 workgroup examines applications pertaining to finance, banking, and insurance. The applications examined by the nine subject matter areas in the Business Method area are explained below.

Subject matter descriptions

Brief description of subject matter

Highlights

Partnership meetings are held each year to engage stakeholders. These meetings allow Technology Center management and participants to share information about initiatives and best practices.

Partnership meeting materials

September 2024 presentation materials

September 2023 presentation materials

September 2022 presentation materials

June 2021 presentation materials

April 2019 presentation materials

March 2018 presentation materials

- Agenda

- 2018 TC Director Update

- 2018 Subject Matter Eligibility Training Update

- Exploring Subject Matter Eligibility Abstract Ideas November 2017 slide deck

- 2018 USPTO Business Methods Panel Discussion About Ex Parte Appeals Synopsis

- 2018 USPTO Business Methods Partnership Speaker Bios

- Referenced Links

- Business Methods Partnership Photos

September 2017 presentation materials

Statistics

This section highlights charts and statistics of the Business Methods Practice Area.

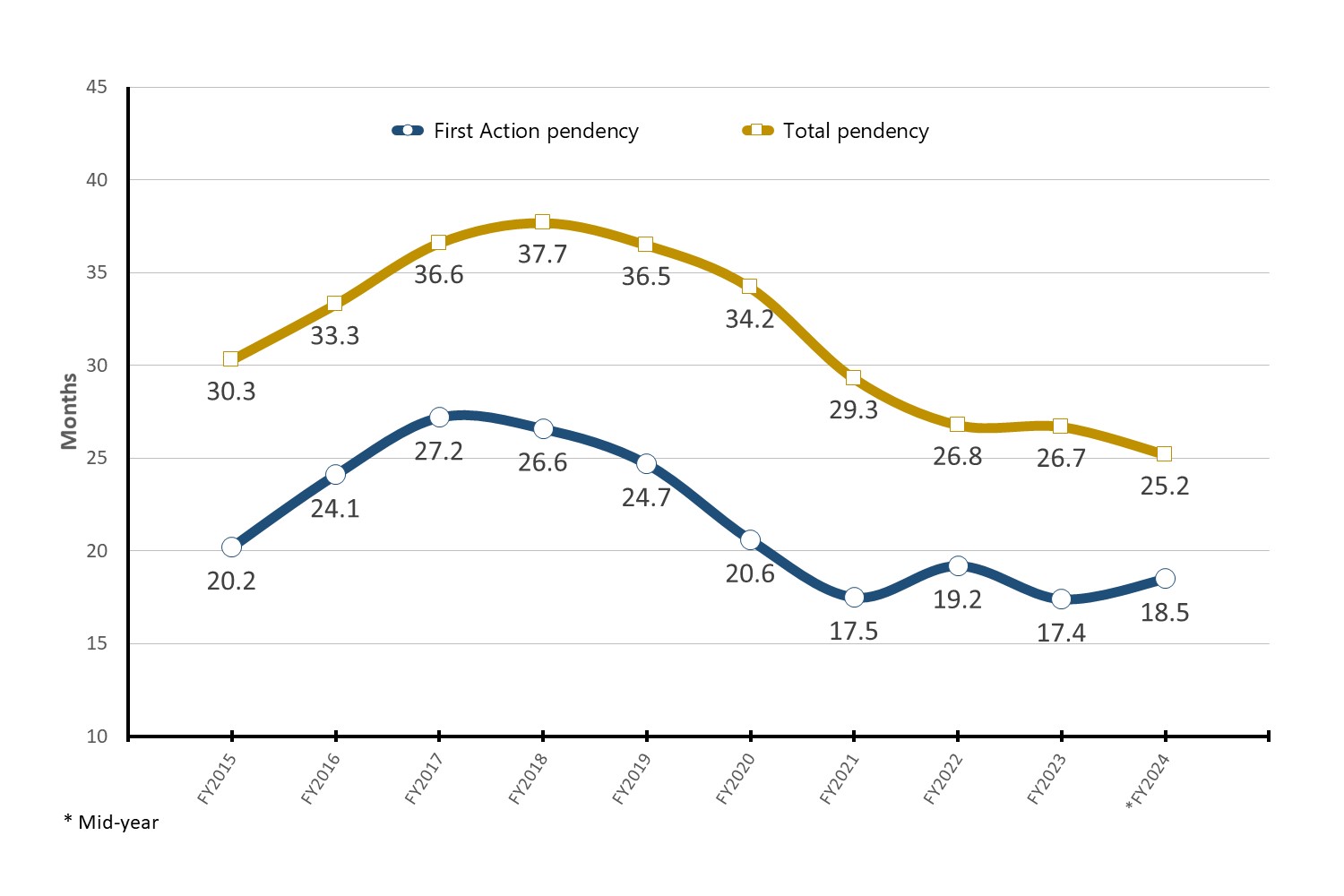

Business Methods pendency

Text version of Business Methods pendency

Statistics published from prior years

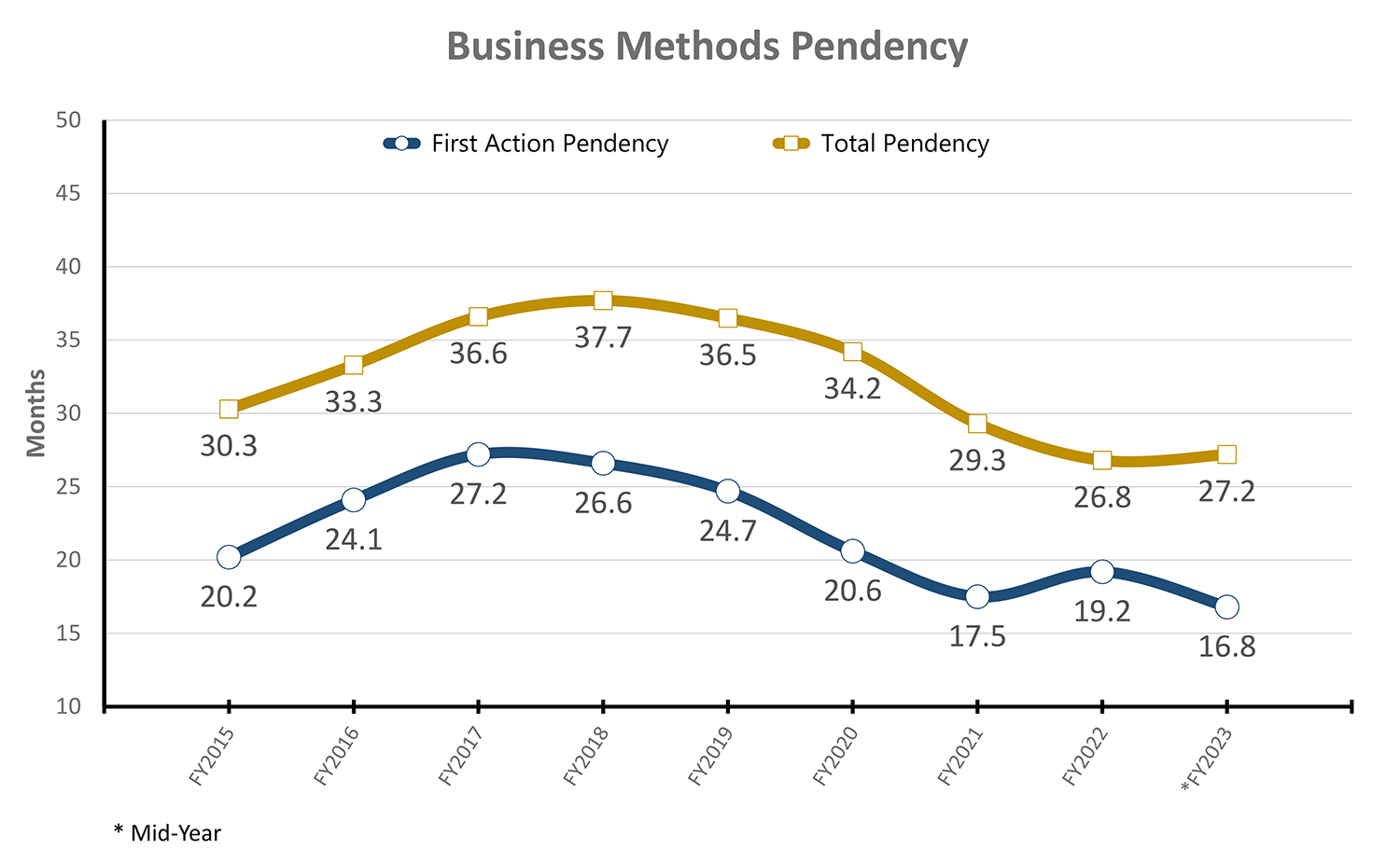

Business Methods Pendency (published 2023)

Text version of Business Methods Pendency

This chart shows the first action and total pendency in the Business Methods area from fiscal year (FY) 2015 to mid-year FY 2023. Overall, pendency has gone down since FY 2018. The first action pendency is down to 16.8 months at mid-year FY 2023 and total pendency is down to 27.2 months at mid-year FY 2023.

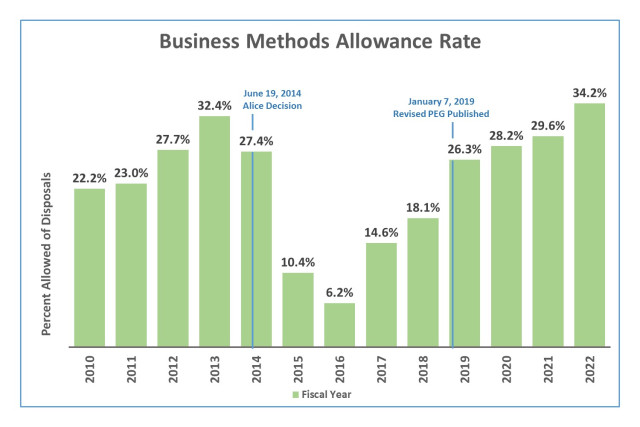

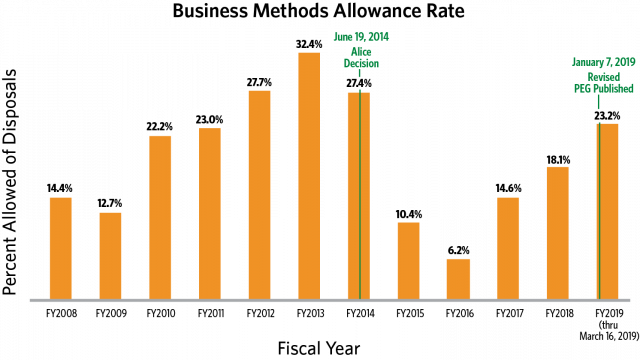

Business Methods Allowance Rate (published 2022)

Text version of Business Methods Allowance Rate

The above graph shows allowance rates of the Business Methods Practice Area currently surpassing the allowance rates achieved prior to Alice Corp. v. CLS Bank International (decided June 19, 2014). Allowance rates are calculated as the number of notices of allowances divided by the number of disposals (including Request for Continued Examination disposals) for fiscal year 2010 through 2022.

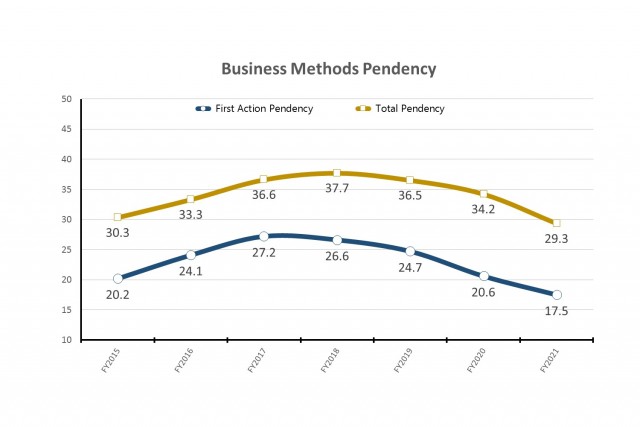

Business Methods Pendency (published 2022)

Text Version of Business Methods Pendency

This chart illustrates the first action and total pendency in the Business Methods area from FY2015 to FY2021. Overall, pendency has been going down since FY2018. The first action pendency is down to 17.5 months in FY2021 and total pendency is down to 29.3 months in FY2021.

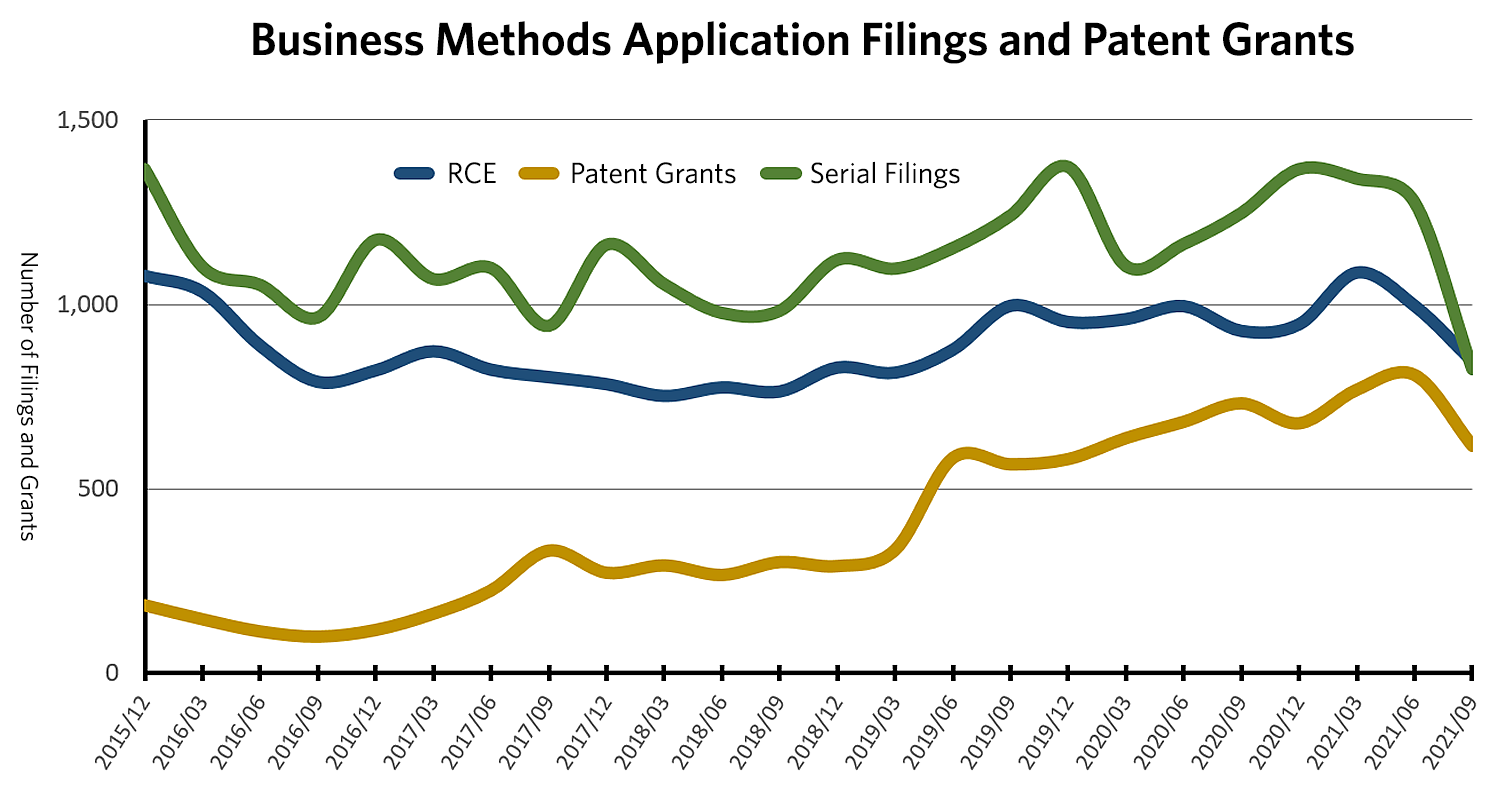

Business Methods Application Filings and Patent Grants (published 2021)

Text Version of Business Methods Application Filings and Patent Grants

The above diagram shows the trend of 3 month average, filings and patent grants for the 6 years 2015 through 2021. It shows the trends for the serialized and RCE filings along with the patents granted during the same period.

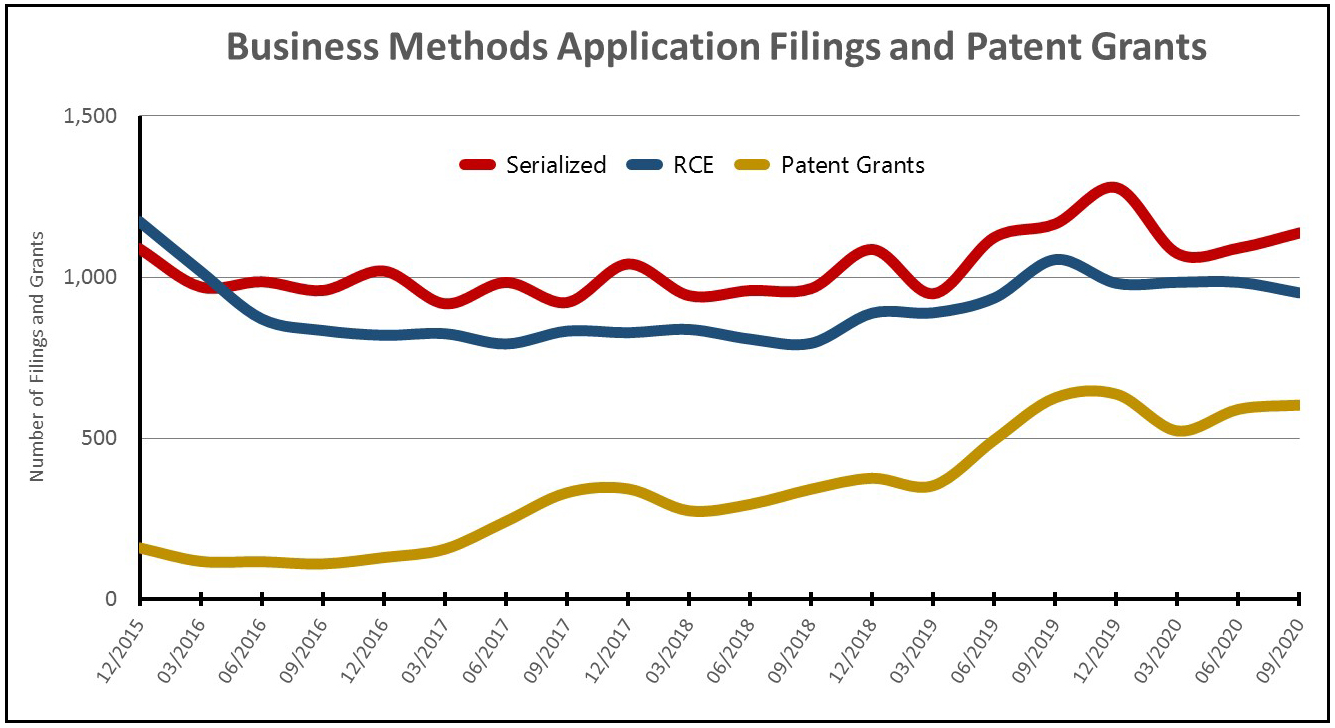

Business Methods Application Filings and Patent Grants (published 2020)

Text Version of Business Methods Application Filings and Patent Grants

The above diagram shows the trend of 3 month average, filings and patent grants for the 5 years 2015 through 2020. It shows the trends for the serialized and RCE filings along with the patents granted during the same period.

Business Methods Allowance Rate 2008-2019 (published 2019)

The above graph shows allowance rates of the Business Methods Practice Area currently surpassing the allowance rates achieved prior to Bilski v. Kappos (decided June 28, 2010) and trending towards the rates achieved prior to Alice Corp. v. CLS Bank International (decided June 19, 2014). Allowance rates are calculated as the number of notices of allowances divided by the number of disposals (including Request for Continued Examination disposals) for each period for fiscal year 2008 through March 16, 2019.

Text Version of Business Methods Allowance Rate

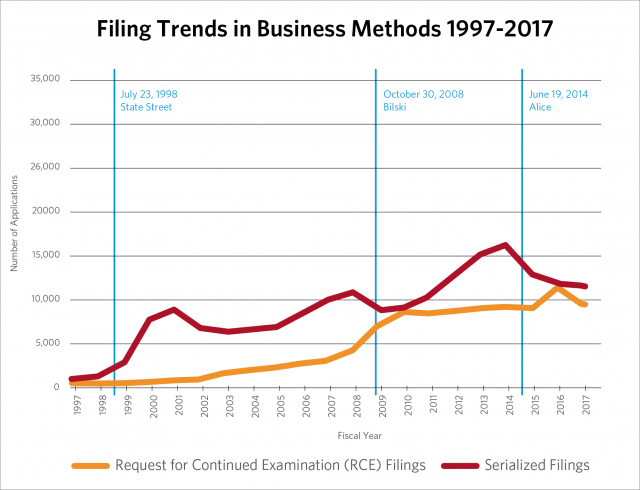

Filing Trends in Business Methods 1997-2017 (published 2018)

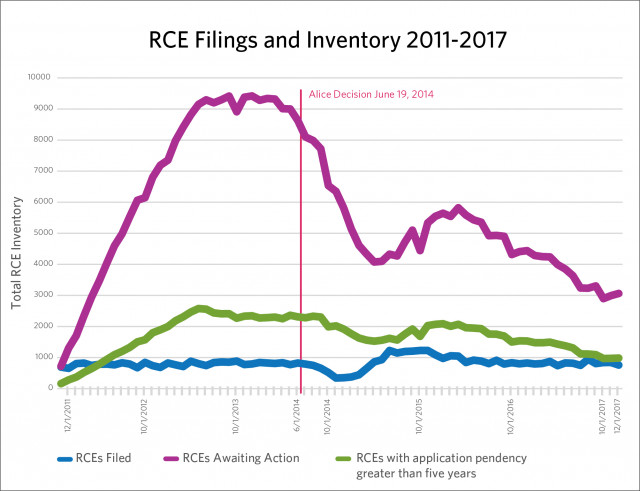

RCE Filings and Inventory 2011-2017 (published 2018)

Between May 1, 2016 and December 1, 2017, the total RCE inventory has steadily decreased despite the RCE filings staying somewhat constant. The total RCE inventory with application pendency greater than five years has also decreased during the same time period.

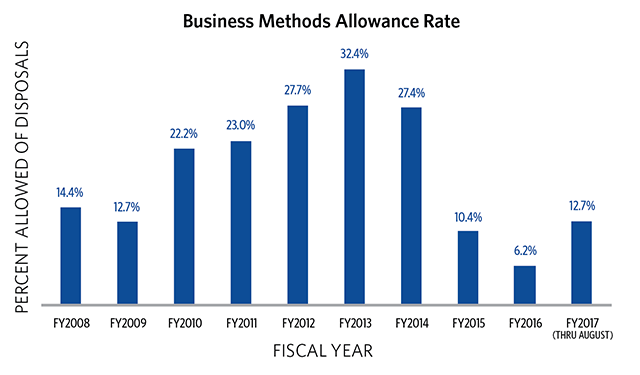

Business Methods Allowance Rate 2008-2017 (published 2017)

The above Business Methods Practice Area Allowance Rate percentages per fiscal year are currently trending towards the allowance rates achieved prior to Bilski v. Kappos (decided June 28, 2010). The allowance rate was calculated as the number of notices of allowance divided by the number of disposals (including Request for Continued Examination disposals) for each period for fiscal year 2008 through August 2017.

Text version of Business Methods Allowance Rate 2008-2017

Guidance and training materials

Below are links to some of the training materials and guidance documents that may be of particular interest to applicants and practitioners in the Business Methods practice area.

35 U.S.C § 101

35 U.S.C § 103

- Examination guidelines and training materials in view of KSR International Co. v Teleflex Inc.

- Developments in the Obviousness Inquiry after KSR International Co. v. Teleflex Inc.

Other examination guidance and training materials

- Artificial Intelligence related patent resources

- Best Practices in Examination

- 35 U.S.C § 112 (a), (b), and (f)

- Claim Interpretation

- America Invents Act

- Patent Trial and Appeal Board

- Practice Tips for Writing Effective Appeal Briefs

Outreach opportunities and presentations

USPTO outreach opportunities bring together inventors and examiners to promote a deeper understanding of technology and the examining process. Find out more about how you can participate in the patent examining process.

- Business Methods Partnership Meetings Speaker Interest Form– Partnering with our external stakeholders to establish a dialogue about mutual topics of interest.

- Patent Examiner Technical Training (PETTP) Program – Opportunities for experts from industry and academia to participate as guest lecturers and provide technical training and expertise to Patent Examiners regarding the state of the art.

- Site Experience Education Program (SEE) Trips – Examiner field trips to commercial, industrial, and academic institutions within U.S. to enable Patent Examiners to explore the technology where it is being developed.

Past Business Methods outreach presentations designed to provide resources and information to our stakeholders

- Business Methods Director’s Dallas Update (August 2018)

- Helpful Tools and Resources (December 2017)

- Business Methods Overview & Highlights from the 2019 Revised Subject Matter Eligibility Guidance (May 2019)

Examiner decision making process

The final say for the determination of patentability resides with the Primary Examiner (MPEP §1004) with the exception of when a Junior Examiner has partial signatory authority (MPEP §1005). The chart below illustrates decision points and who is the deciding official during the first examination, the subsequent examination, and the appeals process.

Text Version of the Examiner Decision Making Process

High level overview of the examiner decision making process

| Decision points | Deciding official |

|---|---|

First  | During first examination:

|

Subsequent  | If a compliant response is filed, then:

|

Appeals process  | If claims have been twice rejected, Applicant may appeal the decision to the PTAB by filing a notice of appeal and an appeal brief. An appeal conference is held with the examiner, SPE, and an additional conferee having sufficient experience to be of assistance in the consideration of the merits of the issues on appeal. The Office makes a decision to re-open prosecution, allow claims, or proceed with the appeal. If a decision is made to proceed with the appeal, the examiner prepares an examiner's answer. |

Contact us

- Tariq Hafiz, Director of TC 3600 Business Methods

- Namrata (Pinky) Boveja, Director TC 3600, Business Methods

- Organizational chart

- Contact us form